From a borrower’s perspective, underwriting is one of the most important steps in the FHA loan process. It can determine whether or not the loan will be approved and funded.

It’s also one of the most “mysterious” steps in the process, especially for first-time home buyers. That’s because buyers usually don’t interact with the underwriter directly. They usually deal with the loan officer or processor, as their primary point of contact.

Not to worry. This guide will walk you through the FHA mortgage underwriting process, including some of the key requirements for borrowers.

FHA Mortgage Underwriting Defined

Before we go any further, we need to clear up a couple of important definitions:

Mortgage underwriting: The process of evaluating a borrower’s financial information and other factors to determine their eligibility for a mortgage loan. It’s a form of due diligence that’s designed to reduce the mortgage lender’s risk.

FHA loan: A government-backed mortgage insured by the Federal Housing Administration. FHA loans offer a relatively low down payment of 3.5% along with flexible credit qualifications.

Put the two together and you have FHA mortgage underwriting.

During this process, a professional underwriter will review the borrower’s credit qualifications, the loan documents, and the property being purchased to make sure they meet the guidelines imposed by the FHA.

The FHA loan program is managed by the Department of Housing and Urban Development (HUD). Detailed mortgage underwriting guidelines and requirements can be found in HUD Handbook 4000.1, also known as the Single Family Housing Policy Handbook.

Mortgage lenders seeking official guidance should refer to the HUD handbook mentioned above. Home buyers, on the other hand, can benefit from a more simplified overview of FHA mortgage underwriting. And that’s what this guide is all about.

What the Underwriter Looks For

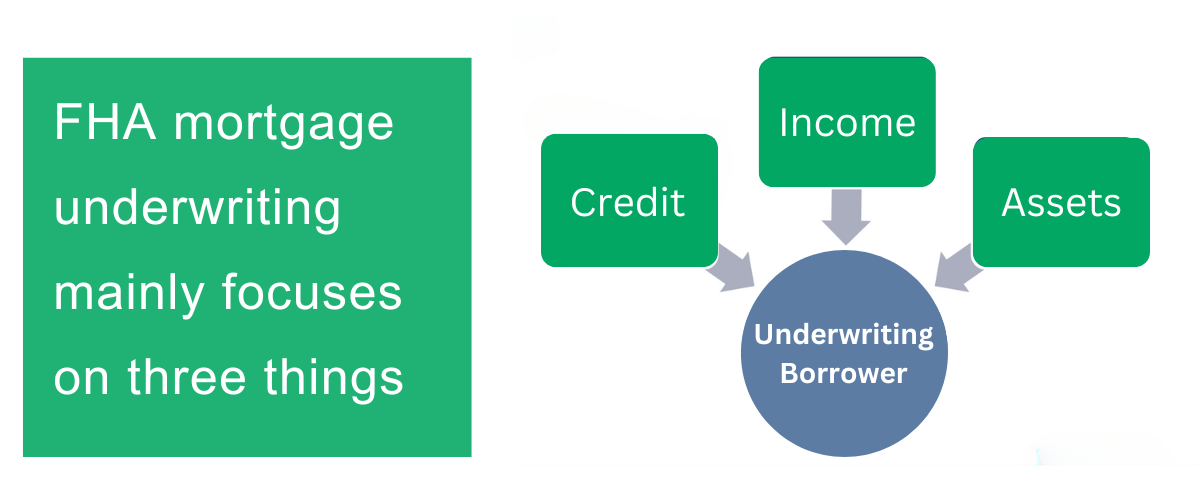

For the most part, FHA loan underwriting focuses on three major areas. The underwriter will review the borrower’s credit history and scores, income situation, and assets.

The underwriter’s primary goal is to make sure the loan is insurable. He or she will check to see if it meets all of HUD’s requirements for the FHA mortgage-insurance program.

Here are some of the things the FHA underwriter will look for during this process:

- Applicant’s credit score

- Debt-to-income ratio

- Employment history

- Income documentation

- Property appraisal

- Loan-to-value ratio

- Compliance with FHA guidelines

- Borrower’s financial reserves

Some mortgage companies have in-house underwriters, or even an underwriting team. Other lenders outsource underwriting to a third-party service provider.

But either way, the purpose is the same. The underwriter’s goal is to ensure that each loan is going to a well-qualified borrower with a high likelihood of repaying, and that it meets the FHA’s guidelines.

If a lender issues a loan that doesn’t meet HUD/FHA guidelines, it may not be fully insured. If the borrower defaults, the lender could incur losses. To prevent this, FHA underwriters review all loan documents for compliance with HUD’s standards.

Two Sets of Criteria: Lender + Government

The underwriter will also check to see if the borrower meets the lender’s minimum criteria.

In order to qualify for an FHA loan, you actually have to meet two different sets of underwriting criteria – the government’s (HUD) as well as the lender’s. Banks and mortgage companies can impose their own guidelines on top of those issued by HUD, and their guidelines might be even stricter.

So the FHA underwriter will look at the loan from an insurance standpoint, to ensure that it meets all program guidelines. He or she must also review the loan documents to make sure the borrower measures up to the lender’s minimum guidelines.

Automated Versus Manual Underwriting

Some FHA loans can be underwritten automatically, through a proprietary software program developed by HUD. That’s the best-case scenario for borrowers, because it expedites the process and signals that the borrower will likely be approved.

In other cases, the software program might flag a loan file and require a more thorough human review. This is known as manual underwriting. In addition to delaying the process, this manual “referral” could require the borrower to submit additional information.

The FHA’s automated underwriting system is called TOTAL Mortgage Scorecard. TOTAL stands for Technology Open To Approved Lenders. According to HUD, it is a “statistically derived algorithm developed by HUD to evaluate borrower credit history and application information.”

Technically speaking, the TOTAL Scorecard is accessed through an Automated Underwriting System (AUS) and is not an AUS itself. But we’re getting into the weeds here.

The point is that all FHA purchase loans must initially go through an automated underwriting system that uses the TOTAL Scorecard algorithm, and some can be flagged for a manual review.

- If a borrower is well-qualified without any “red flags,” they might be approved through TOTAL without the need for human/manual underwriting.

- But in some cases, the TOTAL algorithm will identify an issue and “downgrade” the loan file. This means that a human underwriter must step in and manually review the file.

For instance, a mortgage applicant with an insufficient credit history or a relatively high debt-to-income ratio might trigger a manual underwriting referral. Other factors can cause a downgrade as well.

In short, any time a borrower falls outside of the standard qualification criteria for an FHA loan, they will likely have to go through a manual underwriting review.

Three Possible Outcomes for Borrowers

The underwriting process can result in three possible outcomes. It might help to think of it as a kind of traffic signal, with green, yellow and red lights.

- Green light: The mortgage underwriter finds no problems with the file and issues a “clear to close,” meaning the borrower can proceed to closing.

- Yellow light: The underwriter needs additional information or clarification from the borrower, in order to clear them for closing.

- Red light: The underwriter discovers a serious issue that prevents the borrower from qualifying for an FHA loan.

Stay in touch with your loan officer or broker during this process. Make sure the underwriter has everything they need. And if you do get a list of conditions that must be resolved, act immediately. Otherwise, you might end up delaying your own closing.

What to Do and Expect During This Process

In a typical FHA lending scenario, the borrower does not even hear from the underwriter — at least not directly. If the underwriter encounters any issues, those issues will be passed along to the loan officer who in turn will communicate them to the borrower.

If you’re lucky, you will sail through the process without any snags at all. But don’t be surprised if a few obstacles pop up along the way.

Remember, the FHA underwriter must look at a wide variety of documents and requirements to ensure loan compliance. So there’s a good chance he or she may need additional information to complete the review.

These additional items are commonly referred to as “conditions.” A conditional approval is one that requires additional actions from the borrower, before a final approval can be given.

For example, the FHA underwriter might request a letter of explanation (LOX) from the borrower about a certain bank withdrawal. This is one example of a condition. In this case, the loan might be approved upon successful resolution of this particular issue or condition.

There are a wide variety of issues that can arise during the underwriting stage. It’s the underwriter’s job to determine whether they are resolvable issues or “deal breakers.”

Disclaimers: This guide provides a general overview and therefore does not include every possible FHA loan underwriting scenario. Every mortgage situation is different because every borrower is different. This information has been provided for educational purposes only. As a result, portions of this article might not apply to your particular situation.