Editor’s note: This article was updated in 2024 to include the latest down payment rules and requirements for FHA loans, based on current HUD guidelines. There have been no significant program changes over the past couple of years. The 3.5% rule remains in effect, as explained below.

The FHA loan program is popular among home buyers who don’t have a lot of money saved up for their investment. This program offers a relatively low down payment of 3.5%, for eligible borrowers.

First-time home buyers, in particular, find this appealing. First-time buyers don’t have profits from a previous home sale to put toward their next purchase. So they often struggle to come up with a large upfront investment. FHA loans (and other low-down-payment mortgage options) can benefit such borrowers.

Minimum Down Payment for FHA Loans: 3.5%

The Federal Housing Administration mortgage insurance program is managed by the Department of Housing and Urban Development (HUD). So it’s HUD that establishes all of the guidelines for this program, including the minimum down payment.

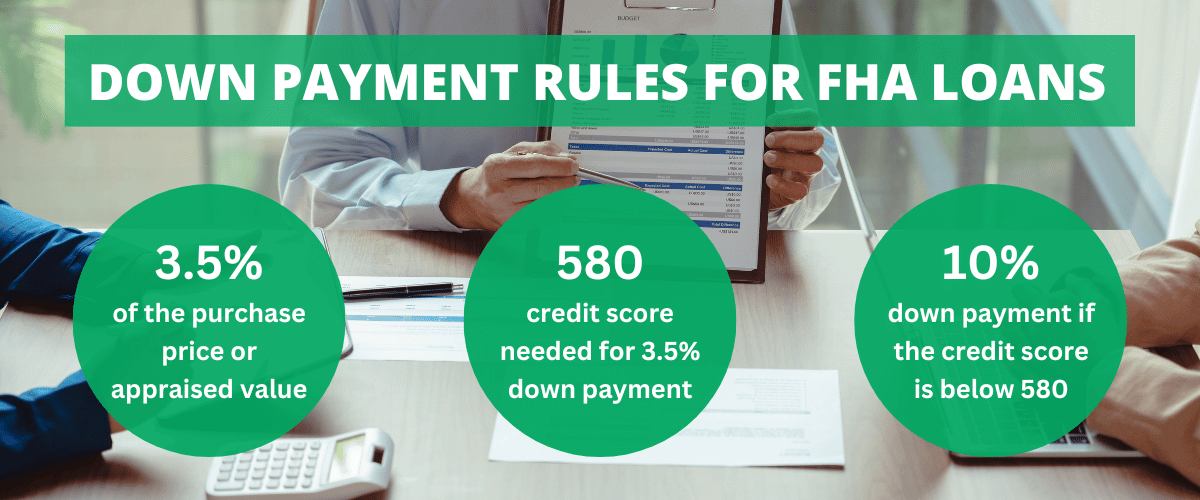

All borrowers who use an FHA-insured mortgage loan to buy a house must make a down payment of at least 3.5% of the purchase price or the appraised value. To qualify for this minimum down payment, borrowers must have a credit score of 580 or higher.

Those are the two most important numbers to keep in mind: 3.5% and 580.

HUD Handbook 4000.1 (the official FHA handbook for mortgage lenders) refers to the down payment as the “Borrower’s Minimum Required Investment (MRI).” Here’s what that handbook says about the MRI:

“In order for FHA to insure this maximum mortgage amount, the Borrower must make a Minimum Required Investment (MRI) of at least 3.5 percent of the Adjusted Value.”

Later, the handbook defines the “adjusted value” as such:

“For [home] purchase transactions, the Adjusted Value is the lesser of: purchase price less any inducements to purchase; or the Property Value.”

Example: If you were buying a home priced at $300,000, you would probably have to put down at least $10,500 in order to qualify for an FHA loan. (The math: 300,000 x .035 = 10,500)

Let’s shift gears now and talk about the loan-to-value ratio, which is another important concept for borrowers to understand.

Maximum Loan-to-Value (LTV) Ratio: 96.5%

In mortgage lingo, the “loan-to-value” (LTV) ratio is simply a percentage that shows how much of the purchase price is being covered by the mortgage loan. For example, if you were to make a down payment of 10% of the purchase price, and you borrowed the rest, your initial LTV would be 90%.

The HUD handbook states the following, in regards to the maximum loan-to-value:

“For [FHA] purchase transactions, the maximum LTV is 96.5 percent of the Adjusted Value.”

You can think of the loan-to-value ratio as the inverse or flip side of the down payment. Borrowers must make an upfront minimum down payment of 3.5% when using this program, which limits them to an LTV of 96.5%.

Credit Score Needed When Putting 3.5% Down

The handbook goes on to state that borrowers need a “minimum decision credit score” of 580 or higher to qualify for the 3.5% down payment amount on an FHA loan.

The absolute minimum credit score for this program is 500. But borrowers with credit scores between 500 and 579 would need to put down at least 10% for FHA. And that removes the primary benefit of using this program in first place.

As a result of this two-tiered credit score and down payment requirement, most of the home buyers who use the FHA loan to buy a house have credit scores of 580 or higher.

- If a person’s “Minimum Decision Credit Score” is 580 or higher, then he or she is eligible for maximum financing up to an LTV of 96.5% — and a down payment of 3.5%.

- If the borrower’s credit score falls between 500 and 579, then he or she is limited to a maximum LTV of 90% — which means a down payment of 10%.

But there’s a catch here. Most mortgage lenders are reluctant to offer financing to borrowers with credit scores in the low-500 range. So even though the official HUD guidelines state that a score of 500 qualifies a person for an FHA loan, the lender might see it differently.

Remember, you’re not borrowing money from the Federal Housing Administration. You’re borrowing it from a lender in the private sector. The loan is only insured by the FHA. So you have to meet the lender’s credit score requirements as well, and they might be stricter than the HUD guidelines.

The Funds Can Be Gifted from a Third Party

Here’s some good news relating to FHA down payments. Federal Housing Administration guidelines allow borrowers to receive funds donated from family members, close friends, or other approved sources. This is referred to as a down payment gift.

So the minimum required investment doesn’t necessarily have to come out of your own pocket. It could be gifted to you from an approved source, which could greatly reduce your upfront out-of-pocket expense. But there must not be any expectation of repayment.

According to FHA guidelines, the home seller cannot contribute money to the buyer’s minimum required down payment. Sellers (and real estate agents, builders, etc.) are considered “interested parties.” Funds provided by interested parties may not be used for the borrower’s minimum required investment (MRI).

Other acceptable sources for down payment funds could include:

- Checking and Savings Accounts

- Cash on Hand

- Retirement Accounts

- Stocks and Bonds

- Private Savings Club

- The Sale of Personal Property

- Gifts From an Approved Donor

Note: Depending on the situation, your lender might be able to accept additional sources not listed above. When in doubt, ask your lender or use the FHA Resource Center hotline.

Frequently Asked Questions From Borrowers

Here are some of the most frequently asked questions we receive from home buyers, regarding FHA loan down payments.

What is the absolute lowest amount I can put down?

As stated above, the absolute minimum down payment requirement for this particular program is 3.5% of the purchase price or the appraised value of home, whichever is less.

What if I can’t come up with the 3.5% that’s required?

Borrowers who cannot come up with the minimum down payment for an FHA purchase loans basically have two options. They can find some other mortgage program that offers a lower investment requirement, or they could obtain some or all of their down-payment funds from a third-party source.

HUD allows gifts from housing agencies, nonprofits, family members, and even close friends with a “documented interest” in the borrower.

You could also look into a down payment assistance program. Nonprofit housing agencies often partner with local governments to provide such assistance programs, which are often geared toward first-time buyers. This is an acceptable down payment source for FHA loans.

Deferred payment loans and grants are the most common types of down payment assistance, but there are other versions as well. Many of these programs are offered at the state and local level, so you’ll have to do some research.

Is it possible to get an FHA loan with no down payment?

No, at this time the Federal Housing Administration does not offer any zero-down mortgage programs. At a minimum, borrowers who use an FHA loan to buy a house must make a minimum investment of 3.5%, which in turn limits the LTV ratio to 96.5%.

Can the down payment be paid in installments?

No, the Federal Housing Administration requires the entire down payment to be paid upfront at the time of closing. However, some state and local housing agencies offer down payment assistance programs that allow borrowers to pay it back over time.

Will the minimum required investment go up in the future?

At this time, we have no indication that the Department of Housing and Urban Development is planning to increase the minimum down payment amount for FHA loans.

Typically, a change like that would be preceded by a considerable amount of discussion, since the Federal Housing Administration is congressionally regulated. We have heard no such discussion, and therefore do not expect them to increase or alter the down payment requirements.

If such a change does occur, we will update this entire website accordingly.