Reader question: “Is it possible to get an FHA loan with a credit score of 500?”

Answer: Technically, a credit score of 500 will qualify you for the FHA loan program. But most FHA-approved mortgage lenders require higher scores (like 600 and up) to minimize risk.

Can I Get an FHA Loan With a Score of 500?

The Federal Housing Administration (FHA) loan program offers an alternate path for borrowers with lower credit scores who cannot qualify for conventional financing.

In addition to making a down payment as low as 3.5%, home buyers who use FHA loans can often qualify for the program even with a history of credit problems.

But there’s a limit to how low your score can be, and those limits can be imposed by both the mortgage lender and the FHA.

Here are five things to know right up front:

- The FHA loan program requires a credit score of 500 or higher for eligibility.

- They also require a 580 or higher to get the low 3.5% down payment option.

- But mortgage lenders that offer these loans can set their own guidelines.

- In 2026, a lot of lenders want to see a score of 600 or higher for FHA loans.

- While a score of 500 meets the official guidelines, most lenders won’t like it.

So yes: you can technically qualify for an FHA-insured mortgage with a credit score around 500. But getting an approval from the lender is a different story.

Minimum Credit Score Requirements

When you first apply for an FHA loan or get pre-approved, your mortgage lender will check your credit score to see if it meets the FHA’s minimum requirements. The lender might even have their own minimum requirements as well, separate from the official ones.

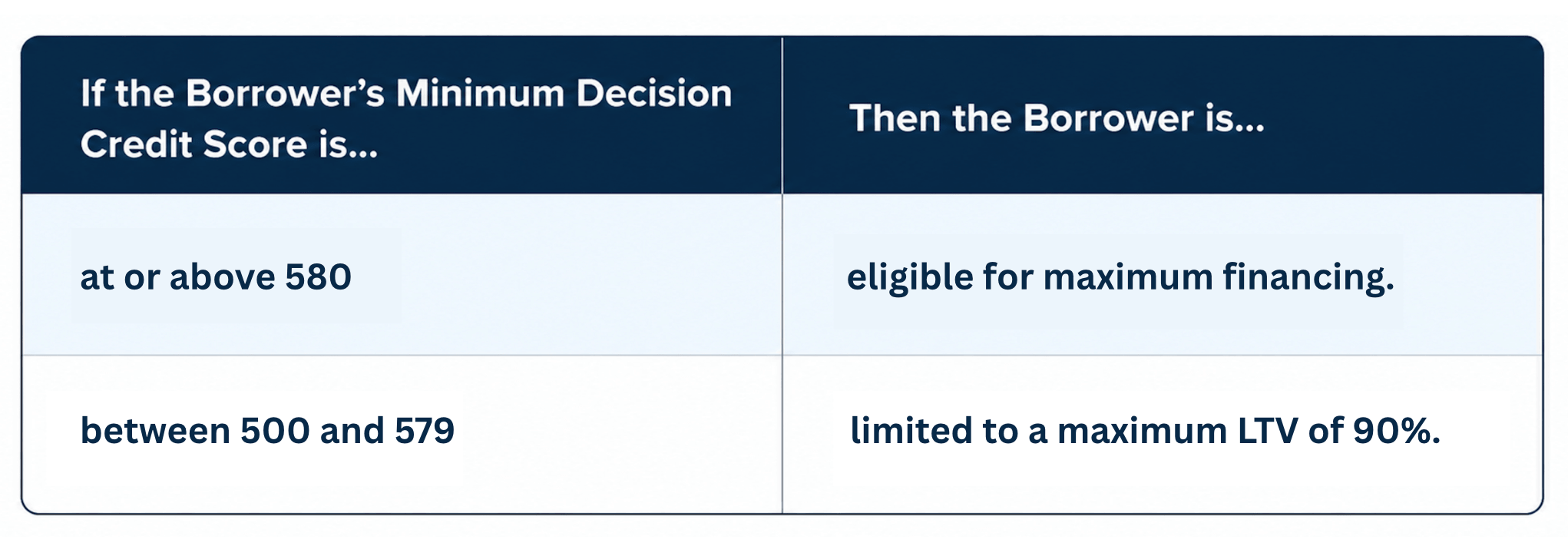

The table below shows the minimum credit score for FHA eligibility and for maximum financing. This table was adapted from HUD’s Single Family Housing Policy Handbook.

(FYI: The Department of Housing and Urban Development, or HUD, manages the FHA loan program and sets all of the rules and requirements for borrowers.)

Here are four important takeaways from this table:

- The FHA generally requires a credit score of 500 or higher for this program.

- Borrowers need a score of 580 or higher for the 3.5% down payment option.

- Borrowers with scores between 500 and 579 might have to put 10% down.

- Borrowers with scores below 500 are typically ineligible for an FHA loan.

In other words: eligible borrowers in the 580-and-up range can get maximum financing up to 96.5% of the purchase price, while those in the 500 – 579 range only qualify for 90%.

To be clear, these are the official requirements established by the federal government. But mortgage lenders can also set their own stricter guidelines, known as “overlays.”

How Mortgage Lender ‘Overlays’ Tie Into This

Most mortgage lenders are reluctant to offer financing to borrowers with credit scores in the low-500 range. So even though the official HUD guidelines state that a score of 500 qualifies a person for an FHA loan, the lender might see it differently.

Remember, you’re not borrowing money from the Federal Housing Administration or HUD. You’re borrowing from a lender in the private sector. The loan is only insured by the FHA. So you have to meet the lender’s credit score requirements in addition to HUD’s.

The truth is, many mortgage lenders set their standards higher than the official program minimums shown in the table above. This is known as an “overlay,” because the mortgage company is laying its own requirements “over” or on top of HUD’s.

Credit score requirements can also vary from one lender to the next. They all have different business models, risk assessment procedures, etc. One lender might require a score of 620 or higher for an FHA loan, while another might allow scores down into the upper-500 range.

Bottom line: The FHA says you need a score of at least 500 to be eligible, and a 580 or higher for the 3.5% down payment. But ultimately it’s the lender’s call, and their requirements can vary. Borrowers with lower credit scores might have to shop around.

Understanding the ‘MDCS’ Terminology

As mentioned, the Department of Housing and Urban Development (HUD) establishes the rules for FHA loans. And according to HUD’s guidelines, mortgage lenders must:

“determine the borrower’s minimum decision credit score (MDCS) … The MDCS will be used to determine the maximum insured financing available to a borrower with traditional credit.”

In other words, your credit score can determine (A) whether or not you qualify for an FHA loan and (B) how much of a down payment you’ll have to make.

Note the term “minimum decision credit score” (MDCS) in the above quote.

Here is how HUD defines the MDCS:

- When the lender pulls three scores (from Experian, TransUnion and Equifax), the middle number must be used for FHA qualification purposes.

- When two scores are pulled (from two of the three credit-reporting bureaus), the lower number must be used to determine eligibility.

- When only one score is obtained, that becomes the MDCS.

At the most basic level, your credit scores show how you have managed your debt and financial obligations in the past, giving lenders a snapshot of how likely you are to repay a loan on time.

Why FHA Loans Can Be More Forgiving

One reason many borrowers explore FHA financing is that it can be more forgiving than conventional mortgage programs when it comes to credit qualifications.

(“Conventional” refers to a regular home loan that’s not backed by any government agency.)

Conventional loans often require stronger credit profiles and can be less flexible when borrowers have past credit issues, such as late payments, collections, or other financial setbacks.

FHA loans, on the other hand, were designed to help expand access to homeownership and generally allow for lower credit scores—among other leniencies.

That’s why some borrowers who cannot qualify for a conventional mortgage might still be eligible for an FHA-insured loan.

Even so, lenders will still review the overall strength of the application, including income, employment history, debt-to-income ratio, and recent credit activity.

Bottom line: FHA loans can be more forgiving, but they still have rules. They generally require a score of at least 500 for eligibility, and 580 or higher for maximum financing.

Five Things to Take Away From All of This

- A 500 score is the official floor. Under FHA guidelines, borrowers generally need a credit score of at least 500 to be eligible for the program. But that does not guarantee loan approval, because lenders can set their own higher standards.

- The 580 mark matters more for down payment. Borrowers with scores of 580 or higher may qualify for the 3.5% down payment option. Those with scores from 500 to 579 typically need a larger down payment of at least 10%.

- Lender overlays can change the outcome. Even if you meet the FHA’s minimum credit score requirement, the mortgage lender could still require a higher score, such as 600 or 620. This is one of the biggest reasons a 500 score can be challenging in the real world.

- FHA loans are more flexible, not automatic. FHA financing can be more forgiving than conventional loans, especially for borrowers with past credit issues. But lenders still review the full application, including income, debts, employment history, and recent credit activity.

- Shopping around may be necessary. Credit score requirements can vary from one mortgage lender to another. A borrower with a lower score might have to contact several lenders to find one willing to work with their situation.