The FHA vs. conventional down payment comparison has become tighter over the last couple of years, due to policy changes made by Fannie Mae and Freddie Mac. These days, eligible borrowers can get a conventional loan with a down payment as low as 3%, compared to the minimum 3.5% that’s required for FHA-insured mortgage loans.

FHA vs. Conventional Loan Down Payments

Once upon a time, the FHA loan program was pretty much the only option for non-military borrowers who were seeking a down payment in the 3% range. (I say “non-military,” because home buyers who are in the military can qualify for a VA loan with zero down payment.) But things have changed.

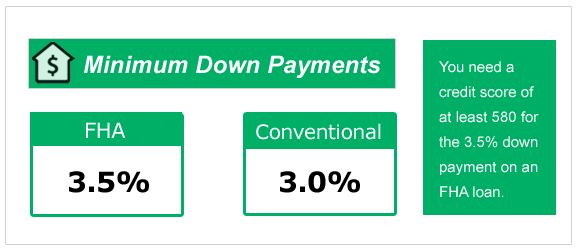

These days, the FHA vs. conventional down payment situation is a much tighter race. Qualified borrowers can now use a conventional loan to buy a home with a down payment as low as 3%. That’s even lower than the minimum required investment for the FHA program, which is 3.5% of the purchase price or appraised value.

We’ll get to the history behind this change in a moment. But first, a brief explainer:

- FHA loans are mortgage loans that get insured by the government. Specifically, they are insured by the Federal Housing Administration, which is part of HUD. This insurance protects the lender (not the borrower) from losses related to borrower default. As a result of this government backing, the minimum requirements for the program can be a bit more relaxed when compared to conventional home loans. The minimum down payment for FHA is 3.5% for borrowers with credit scores of 580 or higher.

- Conventional loans, on the other hand, are not insured by any government agency. They can be insured by private-sector companies (and such insurance is usually required whenever the loan-to-value ratio rises above 80%). But all of this happens within the private sector without any government insurance or backing. The minimum down payment for a conventional loan can be as low as 3% for qualified borrowers.

Policy Changes at Fannie Mae and Freddie Mac

Most of the rules and requirements for conventional loans are established by Freddie Mac and Fannie Mae. They then “trickle down” to the primary mortgage market where home loans are actually originated.

If you’re not familiar with them, Fannie and Freddie are the two government-sponsored enterprises that buys home loans from lenders, securitize them, and then sell them to investors. They have specific requirements for the loans they can purchase from lenders, and one of those requirements has to do with the maximum loan-to-value (LTV) ratio.

Long story short: Fannie and Freddie lowered their LTV limits to 97% over the last year or so. This means that a typical home buyer can now qualify for a conventional loan with a down payment as low as 3%.

As you might have guessed, these down-payment changes have created a shift in market share for both FHA and conventional loans. Industry reports published in 2018 showed that a lower percentage of home buyers were using FHA, while a higher percentage were turning to conventional financing.

In September 2018, for instance, ATTOM Data Solutions published the following insights as part of a quarterly report:

“Residential loans backed by the Federal Housing Administration (FHA) accounted for 10.2 percent of all residential property loans originated in Q2 2018, down from 10.9 percent in the previous quarter and down from 13.5 percent a year ago to the lowest share since Q1 2008 — a more than 10-year low.”

This shift is not surprising, given the LTV limit changes mentioned earlier. There is now a much smaller gap with FHA vs. conventional down payments, and market share has shifted as a result.

Mortgage Insurance: Another Big Consideration

Mortgage insurance is another reason why fewer borrowers are using FHA loans. If you make a relatively low down payment when buying a home, you’ll probably have to pay mortgage insurance. This is true for both FHA and conventional loans.

That’s why some borrowers choose to put down 20% or more. They do it to avoid the 80% LTV “trigger” that brings mortgage insurance into the picture. Of course, not everyone can afford such a large down payment.

But there’s a big difference here:

- Private mortgage insurance (PMI) for conventional loans can usually be cancelled once the homeowner’s LTV falls to 80% or below.

- But with an FHA loan, most borrowers have to pay the annual mortgage insurance premium for the life of the loan.

Bottom line: Conventional loans are now in direct competition with FHA for borrowers who are seeking a low down payment in the 3% range. Still, some borrowers might find it easier to qualify for FHA due to the government backing of those loans.